I have a very simple proposal to boost our high streets again.

Why not insist, or in other words force, legislate, that out of town supermarkets have to open a high street shop, where customers can get service on a limited number of items, and place on-line orders for next day delivery?

In addition supermarkets should fund as many free car parks spaces in the town as they have at their out of town location.

Sound fair doesn't it, that is if we want to rejuvenate our town centres.

Tuesday 20 December 2011

Sunday 18 December 2011

Shared debt and the ECB

So finally some sensible people are beginning to acknowledge that the euro issue cannot be solved by tough budgets.

No, the most urgent things are:

1 Sharing the debt. The euro countries cannot any more go their own way with Germany benefiting and Greece dying. There has to be shared debt burden and responsibility.

2 ECB as a lender of last resort. The ECB has to become the euro central bank, fully engaged in all the necessary banking activities that other central banks do.

Just those two simple things and the euro can become a valid currency. Without them it is just going to drag on and on, before eventual collapse.

No, the most urgent things are:

1 Sharing the debt. The euro countries cannot any more go their own way with Germany benefiting and Greece dying. There has to be shared debt burden and responsibility.

2 ECB as a lender of last resort. The ECB has to become the euro central bank, fully engaged in all the necessary banking activities that other central banks do.

Just those two simple things and the euro can become a valid currency. Without them it is just going to drag on and on, before eventual collapse.

Saturday 17 December 2011

Where does the economic problem lie?

Here's some thoughts

Globalisation. Which has undermined the manufacturing base in our economy, caused loss of jobs and falling living standards. It is USA & Europe versus China & India. But we brought it on ourselves by moving those jobs to Asia and giving them our technology!Government paralysis. Powerful interests prevent action on un-employment (freezing up of loans), inequality (poor incomes) & budget deficits (bond yields?). Our top income tax is too low, so their is not enough equality in society. Our banks are under-capitalised and un-regulated as we don't insist on either. Public investment is strangled and miss directed to structural spending not productive investment. The poor are asked to pay for the errors of the rich.

Politicians are in over their heads. They are arts graduates, not economists or technologists. So special interest groups move in and write the agenda. EU summits all fail politically and technically. The euro is being killed by incompetence.

No policy. The USA has miserably failed to produce any policies on any major item: budget, tax, energy, climate, financial regulation, healthcare or property. Europe is likewise lacking democratic policies that will work. The EU's 27 nations all await only Germany's proposals, which themselves are driven by a disaster of coalition politics, crippled banks, local interests and amateur politicians. The EU commission itself has no role and has done nothing. Treaties are pushed forwards with no debate, technical or political, the EU parliament is sidelined and has a huge democratic deficit as local parliaments hang onto power.

Fundamental problems. The two fundamental problems are inequality and poverty, these need active government policies of equality and inclusion. But current policies are trending to support the rich and penalise the poor. OUR money is being consistently sucked from us to fund casino banking. De-capitalised banks, through stupid investments of their own and central policy, fail. While Europe as a whole gets no focus on fiscal controls and central banking needs, while banks continue to worsen.

Despise Government. Perhaps the worst of all, as long as this goes on people will more and more despise Government and politicians on TV. They present no solutions. We need to make democracy work again, educate people to make decisions, present the options and ask them to decide. For our sake.

Thanks to the Guardian for stimulating me to write this.

Wednesday 14 December 2011

Time for some facts - euro mess

The BBC has published these charts, chosen by economists to show the situation we are in

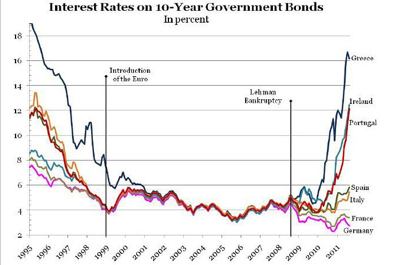

This for me is the most interesting, as it is long term. As you can see Greece had a BIG cost of raising loans before the euro, during the euro just about everyone could borrow at the same rate - never mind their underlying fiscal position! Then after the bust everything went pear shaped and those that had borrowed more than they could possibly pay off have been hit with high interest rates - how stupid of them.

This for me is the most interesting, as it is long term. As you can see Greece had a BIG cost of raising loans before the euro, during the euro just about everyone could borrow at the same rate - never mind their underlying fiscal position! Then after the bust everything went pear shaped and those that had borrowed more than they could possibly pay off have been hit with high interest rates - how stupid of them.

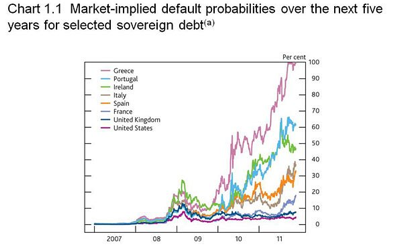

And so now many countries are rapidly approaching the point where default will happen. And good luck to them when that does. The problem is they may take everyone else with them.

And so now many countries are rapidly approaching the point where default will happen. And good luck to them when that does. The problem is they may take everyone else with them.

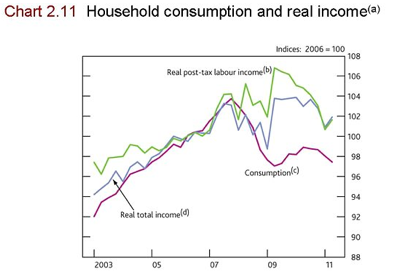

The economy is tanking because households are not spending, in fact as we see below everyone is irrationally saving - or maybe it is because banks are charging too much interest - 20% on a credit card is much too much! Especially when the BOE rate is near zero.

The economy is tanking because households are not spending, in fact as we see below everyone is irrationally saving - or maybe it is because banks are charging too much interest - 20% on a credit card is much too much! Especially when the BOE rate is near zero.

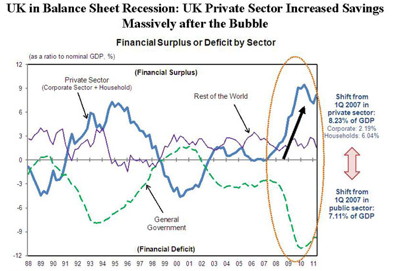

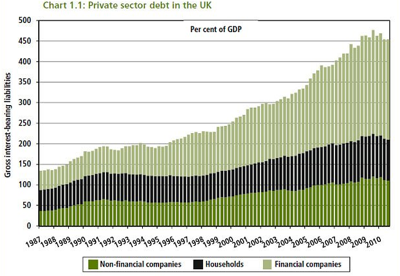

But the thing is, it's not government debt which is out of control, although it is bad enough because too much of it is expenses (health, social, education) not investment (roads, trains). Nor is it the finance companies. It is the households and non-financial companies that have huge debts.

But the thing is, it's not government debt which is out of control, although it is bad enough because too much of it is expenses (health, social, education) not investment (roads, trains). Nor is it the finance companies. It is the households and non-financial companies that have huge debts.

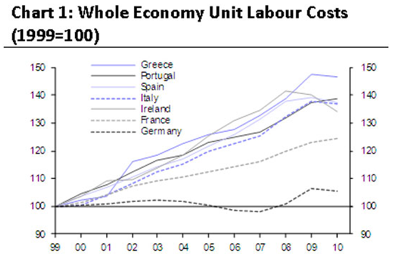

So why did Greece and the other go belly up? Relative labour costs! And lack of productivity. Unfortunately the UK is not on this chart, so it is finger pointing at the euro zone, but hey-ho it gives their game away.

So why did Greece and the other go belly up? Relative labour costs! And lack of productivity. Unfortunately the UK is not on this chart, so it is finger pointing at the euro zone, but hey-ho it gives their game away.

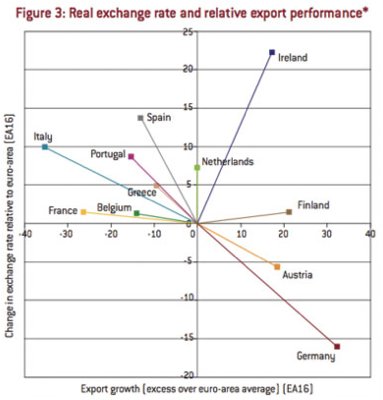

Last the relative competitiveness of different countries. The vertical column shows what the exchange rate should be against the euro plotted against the export growth which essential to survive. As you can see Germany has profited greatly by effectively having a too cheap currency and exporting greatly, whereas poor old Italy should have a lower currency and needs to do a whole lot better exporting.

Last the relative competitiveness of different countries. The vertical column shows what the exchange rate should be against the euro plotted against the export growth which essential to survive. As you can see Germany has profited greatly by effectively having a too cheap currency and exporting greatly, whereas poor old Italy should have a lower currency and needs to do a whole lot better exporting.

So there it is, now we just need everyone to get educated to read and understand these things so we can stop stupid political eurosceptic red-top paper headlines.

This for me is the most interesting, as it is long term. As you can see Greece had a BIG cost of raising loans before the euro, during the euro just about everyone could borrow at the same rate - never mind their underlying fiscal position! Then after the bust everything went pear shaped and those that had borrowed more than they could possibly pay off have been hit with high interest rates - how stupid of them.

And so now many countries are rapidly approaching the point where default will happen. And good luck to them when that does. The problem is they may take everyone else with them.

The economy is tanking because households are not spending, in fact as we see below everyone is irrationally saving - or maybe it is because banks are charging too much interest - 20% on a credit card is much too much! Especially when the BOE rate is near zero.

But the thing is, it's not government debt which is out of control, although it is bad enough because too much of it is expenses (health, social, education) not investment (roads, trains). Nor is it the finance companies. It is the households and non-financial companies that have huge debts.

So why did Greece and the other go belly up? Relative labour costs! And lack of productivity. Unfortunately the UK is not on this chart, so it is finger pointing at the euro zone, but hey-ho it gives their game away.

Last the relative competitiveness of different countries. The vertical column shows what the exchange rate should be against the euro plotted against the export growth which essential to survive. As you can see Germany has profited greatly by effectively having a too cheap currency and exporting greatly, whereas poor old Italy should have a lower currency and needs to do a whole lot better exporting.So there it is, now we just need everyone to get educated to read and understand these things so we can stop stupid political eurosceptic red-top paper headlines.

Tuesday 13 December 2011

Banks, vital?

Just a few numbers

Finance sector employs 1m people, add to that hangers on you get maybe 1.5m. 80% work in retail high street banks (a service industry).Manufacturing employs 2m people (productive industry)

Tax paid by finance sector (2002-9) was £193bn, but manufacturing paid £378bn

IMF says tax payers paid £289bn to prop up banks since 2008. Add in government underwriting and loans and you get £1.19tn

In 2007 40% of bank and BS lending was on property, 25% went to financial intermediaries. So 65% of lending went to pumping up the bubble

The City now pays more than 50% of Conservative party funds, up from 25% only 5 years ago.

So there we have it, dysfunctional capitalism.

And does anyone think we need less control of the banks?

If they will not redirect their activities to productive investment then they must be forced to do so, or pay the piper a Tobin Tax.Monday 12 December 2011

A new rage against the BBC and Flash

The BBC has closed its iPlayer site that allowed us to comment, question and complain about iPlayer,

But I have not forgotten one of the major complaints. The widespread use of Flash to distribute both sound and video. This is deeply embedded in the BBCs technology, and is deeply annoying for customers who have, rightly, turned they back on Flash and moved to the new open HTML 5 standard, 99% of users of which use H264 for video and AAC for audio. H264 by the way is a standard for video that is compatible across all platforms, it is used in mobile phones, tablets, digital TV, HD TV whereas Flash is closed an propriety and licensable if you want to use it...Why not HTML5/H264 for all versions of the iPlayer?

I cannot for the life of me why the BBC clings to the old Flash implementations of iPlayer. On the iPad it is streaming H264, but try to access it on your PC and you get Flash, which if like me you do not have Flash installed, means that I cannot view iPlayer on my MacBook..This is absurd. Maybe, just maybe, as they won't admit that this has been forced upon them by media companies scared of people copying programs, and re-distributing them on the Internet. But this is a silly argument, all programs are publicly broadcast, they can be recorded on DVRs and could then easily be transposed to H264 and put on the web. Moreover at least two companies (CatchupTV and FilmOn) are retransmitting live TV using iPad compatible video formats.

Another grouse. The BBC iPlayer app on the iPad does not allow video to be streamed to my TV via the small Apple TV box (which receives media by WiFi and outputs HDMI). Other companies regard this as a major advantage, to be able to offer their content on the Home TV (see TED and many others). In fact the stupidity is even worse, as my Sony TV has internet connectivity and a version of the BBC iPlayer on it, so I can get full screen viewing through this route, but why not from the iPad? The only problem is that my TV needs a wired Ethernet connection!! Not just WiFi. I object, no more wires!

The BBCs attitude just beggars belief, they have spent million on technology, but are way outside the trend. Time to catchup BBC.

As I see it now, the euro crisis

It has not gone away!

First, let's be clear UK did not exercise a "veto", if it had been a veto then the policy would not go ahead, at least not within the EU organisations… Cameron simply walked away. This leaves 26 countries to form a new EU group, with us on the outside. No one in their right mind could think this new group will not find a way to use the EU institutions (Council, Commission, ECB, Courts) to work for them… resulting in a constitutional crisis and working paralysis…Next, there is still no protection at all for our "financial industry" (remember the guys who got us in this mess in the first place…) as new finance regulations within the EU (of which remember we are a part) will be imposed by majority voting. This seems 100% certain as 26 of the 27 have expressed their intention of grouping together to solve the finance crisis.

Next, The Lib Dems are right. We need to be strong, and be inside the EU. We are, whether we like it or not a part of Europe, there's no where else for a small, broken country to go…

Next, the agreement may fix the deficit problems and agree the 3/60% rule by legal means - whatever the economic consequences for poor Greece and the others - probably this will create a severe depression…

But, they have not solved the debt problem. The huge sovereign and bank debts remain. The small bazooka of various funds will not cure the problem, as it is unbalanced unless a common euro bond is issued to balance all the countries in one group.

So, now let's see what happens next…

Sunday 11 December 2011

The UK problem

How on earth can UK be a strong member of the EU, creating and defining policies and governance, if we consistently stay out of it?

Conservative do not participate in the EU parliamentary party. We have separate and much ignored election of unknown EU politicians. We do not accept to transfer power to the EU parliament or the EU Commission, and live with EU management only through dictatorial power of the commission and democratic rubber stamping by the EU Council (heads of state meetings…). There has to be another way, it may be radical but we should get fully stuck-in and adopt a future that is European.

Conservative do not participate in the EU parliamentary party. We have separate and much ignored election of unknown EU politicians. We do not accept to transfer power to the EU parliament or the EU Commission, and live with EU management only through dictatorial power of the commission and democratic rubber stamping by the EU Council (heads of state meetings…). There has to be another way, it may be radical but we should get fully stuck-in and adopt a future that is European.

Two problems

Shake out.

One of the shake-outs from the big EU meeting last week was to delineate the TWO problems, only on of which has been addressed.1 Deficits. Without a doubt many EU countries have unacceptable and unsustainable deficits. These cannot be cured overnight, and as far as I know the meeting did not define a timescale for them to be fixed. Personally I think 20 years might be a good frame to think about.

2 Debt. Many big nations have huge debts, including the USA, and all of the EU. The problems of debt is borrowing, and the problem of borrowing is that lenders demand an interest on their money. And for many EU countries this interest is getting too large, as lenders are beginning to believe that debts may not be repaid and default could happen. In other words a country is in sovereign debt where its whole wealth is not enough to pay its debts, and it is continuously running up more by overspending.

Debt comes about only when lenders agree to lend to borrowers, both create the debt, both are responsible, this means the banks. Today EU banks carry too much debt, by lending to countries who increasingly can't pay. The question is how to get enough money to pay off the debts, as the countries cannot generate enough to do it, considering the interest that the loans demand. In the USA the FED simply prints more money, in UK the Bank of England (why not the Bank of UK?) gives money to banks called quantitive easing. But in the EU there is no bank to do this, the ECB charter does not allow it to do it as there is no central financial management.

So the question remains.

We have proposals to have a treaty to coordinate every countries budgets, to solve the first problem - expect for UK which walked away from the table. But for the second - where will the money come from that is urgently needed NOW - there is no solution.Saturday 10 December 2011

The Apple magic has gone?

I am feeling a bit down today.

Why? Because I have been reading blogs about Apple and its products, and I have even gone back to browsing their web site, and I am not moved to want anything new from them.No more magic? What could have happened?

Maybe it's just that the new iPhone 4S (which my son has, and I am not jealous) looks just the same as the iPhone 4 (which I have). Siri just makes me feel foolish, talking to a phone, indeed.Maybe its because I am a little underwhelmed with the performance and features of iCloud.

- OK so after a while my photos do appear in iPhoto, but only when I am on WiFi, I want them over 3G (I have an unlimited contract from "3", very good value!).

- My Pages docs do not sync to Pages on my MacBook (nor do Keynote or Numbers files).

- I will not have , after July 2012, a Mobile Me web site - that is a real negative.

- Having email that syncs across devices is not new, I had that years ago using IMAP technology, deleting an email on my iPhone or iPad deletes it on my MacBook before I have a chance to decide if I want to file it away…whoops, and I can't transfer files saved on my MacBook back to the iPad/iPhone, in fact I can't see my FILING folder at all.

Maybe it is because I see Apple as not responding to markets outside the USA in terms of product conception and performance offerings? They seem tied to the coat tails of AT&T in the features of the iPhone, whereas in Europe our networks are cheaper and more open.

Maybe because I simply don't believe they could get anywhere with a standard TV. They could perhaps make a better box like EyeTV (e.g. a receiver with WiFi output) , but there are so many world standards for TV distribution that I wonder if this could be possible? If they want to do everything over the internet, that's fine, but the network capacity in UK, at least, is not up to it, and the competition from BT (who, remember own the network!) is strong and maybe favoritised?

Maybe because they seem to not be getting their way with the media companies and studios in the way they used to when iTunes started. Their Movies, TV shows and Books all are behind the latest tends and studios still show films in cinemas first, then DVD then iTunes, by which time there is no more interest (that's why we have pirates). There is no excitement in the offering. You can't just keep flogging the Beatles!

I am becoming disappointed in my iPad (v 1.0) as Safari and now the new iBooks apps keep crashing back to the home screen, why? Is the focus on iPad 2 with not enough testing on the older iPad 1?

Maybe because the damned Samsung seem to be getting away with blatant stealing of Apple's IP, and copying the look and feel of the iPhone and iPad.

But I have to say that I am well content with OS10 Lion on my 4year old MacBook. I don't have track pad gestures, but otherwise it runs fine. A bit more processing power and memory (I am maxed out at 2GB) would help when I have 4-5 apps running in full screen. And I am truly annoyed at iPhoto not having an import capability in full screen mode!

I do hope Apple will regain their leadership and innovative idea-block they seem to be going through. They need a new market to revolutionise… TV could be one, but how without media cooperation? Low cost PC could be another (sort of iPad with keyboard) to finally knock some competitors out of the market (not innovative I know, but a better product)… HD audio, now there's a market waiting to happen, Apple could re-awaken everyone's appreciation of high quality audio (quality over quantity), knock a hole in Amazon's MP3 stuff, and awful offerings like Spotify streaming (quantity over quality approach). The could make a lot more of Airplay, bit getting more makers to implement it, raising the audio bar to transmit 24bit/96kHz audio, insisting that any app on iPad should be able to stream both audio and video (again this means getting the initiative back from media people, like the BBC whose iPlayer only streams audio to my Apple TV!).

Friday 9 December 2011

How is the UK doing?

Debts, debts debts

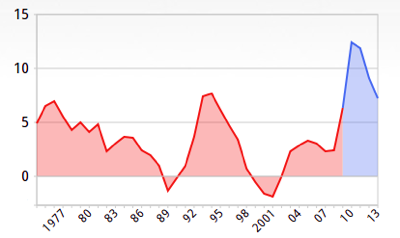

Deficit as a % of GDP. (EU Treaty limit is 3%)

Deficit as a % of GDP. (EU Treaty limit is 3%)

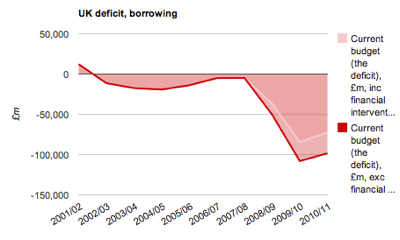

To fund it, the Government borrowed a monumental £170.8 billion last year. If all goes well, we're set to borrow another £167.9 billion this year. With government spending so far out of control, interest on the national debt will cost over £42 billion this year.

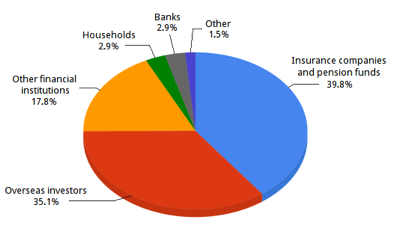

To fund it, the Government borrowed a monumental £170.8 billion last year. If all goes well, we're set to borrow another £167.9 billion this year. With government spending so far out of control, interest on the national debt will cost over £42 billion this year. This is who owns our debt. Currently just over 35% of our national debt is owed to foreign governments and investors. So it's not just Third World nations in hock to the rest of the world. We're relying on the confidence of foreign investors to keep our own country afloat. According to EU figures, Britain has pledged £781.2 billion in capital injections, liability guarantees and liquidity support to the banking system. As taxpayers, we're on the hook for any losses.

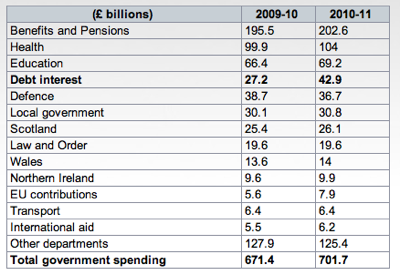

This is who owns our debt. Currently just over 35% of our national debt is owed to foreign governments and investors. So it's not just Third World nations in hock to the rest of the world. We're relying on the confidence of foreign investors to keep our own country afloat. According to EU figures, Britain has pledged £781.2 billion in capital injections, liability guarantees and liquidity support to the banking system. As taxpayers, we're on the hook for any losses. This is what we spend our money on. In 2010-11, interest payments on the national debt will be the fourth biggest line in the budget, reaching £42.9 billion.

This is what we spend our money on. In 2010-11, interest payments on the national debt will be the fourth biggest line in the budget, reaching £42.9 billion.There is productive and non-productive spending. Public spending is set to rise by £119 billion between 2008 and 2011. Just 6% of this is associated with capital investment. Another 38% is a result of higher social security bills during recession and the dead money of debt interest. This leaves the remaining 56%, which the Government is willfully borrowing to fund yet more unproductive consumption.

Last year national debt interest cost the taxpayer £27.2 billion. In 2010-11 that figure soars to a jaw-dropping £42.9 billion. The more we spend on interest, the less we have to pay down debt or invest for the future. That interest is dead money, which means higher taxes for years to come.

Europe as I see it now

EU DISASTER, UK DISASTER

So last night they met, and they had a nice dinner and a few glasses of wine, and they tried to sort out the money mess that they have got the rest of us into. The EU treaty clearly says that debts must be 3%/60% of GDP, and so far everyone of the EU countries signed up to this has broken the treaty agreement, just shrugging their shoulders at it. So much for treaties. Or lack of oversight by the EU commission and/or EU courts.Can anything change? Well they held the meeting and...

Cameron did NOT use his "veto", he just put a proposal on the table which was not accepted by most other states. We all agree that our debts have to be brought down to manageable levels, and he could have agreed with that. But to insist that the UK finance industry is protected above that of other European countries is unadulterated protectionism and abound to be rejected.

His negotiating tactic also was stupid, he confused this meeting with a meeting of the EU Heads of State under the EU commission aegis, it was not, it was a meeting of countries about their financial crisis - of which UK is a big part!

The first proposal was to have the EU change its treaty to put in the financial policies (debt levels, central financial governance….), this was not agreed by all countries, and not by Cameron without an opt-out clause protecting our finance industry.

So proposal number two was to have a smaller grouping of countries using the euro, and some others who might join the euro some day, and these countries would form a pact to work together.

He did not now have a "veto" at this meeting, just the chance to moan about some special protocols for UK, seeing that the meeting's outcome was not a treaty change for the whole 27 countries of the EU. This idea was now dead in the water.

So, it was not a proposed treaty change for the EU, as other countries did not agree or had to go back and consult. It is just a "private" agreement among those euro countries who signed up, and possibly some others. In this Cameron did not have a "veto" and any request for protection for UK finance industry has no part.

Now he is in dire trouble. He is stupidly supporting the finance industry (against the strong push being made in UK government by the Liberals to support manufacturing, not finance!), he is being pushed by euro-skeptics to demand concessions, but these are not on the table. He is damned if he does and damned if he doesn't. If he back peddles and agrees now to accept the proposals and get them implemented at EU level, then he may have to call a referendum, if he still walks away saying he does not agree, then he has contributed to a two-speed europe, where the UK is in a small minority, on the outside.

Thursday 8 December 2011

Excuse me, but both governments AND banks are guilty

Excuse me but can I ask a question?

How come the banks can loan any amount of money, at an interest rate they demand, to countries that are in contravention of the Maastrich Treaty (3% deficit and 60% debt, to GDP)?Are they totally immoral or, in my belief, illegal in doing so. I really don't see why they should not have just turned round and said to countries outside the parameters of the EU treaty (not just the euro zone!) that they will not extend any more credit. To extend credit outside the limits is to gamble with our sovereignty and I am sure no one of us would agree with that. It was, and is, wrong to believe that they can go on expanding their loans, and thus making more and more profits, from exploiting us, we the people.

Both sides are guilty

So, let's start putting the blame in both places where it belongs. Sure governments (not "politicians", but elected governments) have sought to break the rules and gone about spending that they could not afford, but the banks are equally guilty in making the loans.Tuesday 6 December 2011

Go Cameron, Go

David Cameron, far from being in a noose over the EU and the euro - supposedly tightened by the so-called euro-sceptics, is actually in a great position.

Provided! He grabs this opportunity for the UK to be a strong reforming force in the EU. What do I mean by that?

- He should take a strong stand about the successful future of the EU and the wide adoption of the euro.

- He must avoid the temptation to just do what the city wants, he must do what, us, the people want. Fairness, equality, care… sovereignty of our money…

- He should indicate that, if reforms go ahead and markets are suitable then the UK will join the euro.

- He should "join them" not "stand apart", the UK has a huge amount to offer to the ongoing proposals, we started our efforts to reduce our budget deficit a while ago, others are just starting. His advice on how to go about it is invaluable.

This is the politics of international relations, the USA (including its S&P, Moody's and other rating agencies) is already in decline and no longer able to bully the world over how things should be run. China is budding, but the EU has all the ability to take a leading position in the world. Just let's get it right.

The basic operating methodology of financial markets (mathematical calculation of risk, association of risk and interest, deep levels of CDS on loans…) has to be challenged by governments who are acting for their people. Our sovereignty has an indeterminate value, not a fixed value appointed by financial organisations.

Not that this means governments can run up huge debts, they cannot and must be stopped from doing so. But this has to done throughout the EU not just to sustain the euro as a currency, that is a consequence not a cause. We need to take 20 years to solve the debt problem, not a week that financial markets would like to see to sustain their ridiculous short-term culture.

Provided! He grabs this opportunity for the UK to be a strong reforming force in the EU. What do I mean by that?

- He should take a strong stand about the successful future of the EU and the wide adoption of the euro.

- He must avoid the temptation to just do what the city wants, he must do what, us, the people want. Fairness, equality, care… sovereignty of our money…

- He should indicate that, if reforms go ahead and markets are suitable then the UK will join the euro.

- He should "join them" not "stand apart", the UK has a huge amount to offer to the ongoing proposals, we started our efforts to reduce our budget deficit a while ago, others are just starting. His advice on how to go about it is invaluable.

This is the politics of international relations, the USA (including its S&P, Moody's and other rating agencies) is already in decline and no longer able to bully the world over how things should be run. China is budding, but the EU has all the ability to take a leading position in the world. Just let's get it right.

The basic operating methodology of financial markets (mathematical calculation of risk, association of risk and interest, deep levels of CDS on loans…) has to be challenged by governments who are acting for their people. Our sovereignty has an indeterminate value, not a fixed value appointed by financial organisations.

Not that this means governments can run up huge debts, they cannot and must be stopped from doing so. But this has to done throughout the EU not just to sustain the euro as a currency, that is a consequence not a cause. We need to take 20 years to solve the debt problem, not a week that financial markets would like to see to sustain their ridiculous short-term culture.

Sunday 4 December 2011

Putting PDF slide shows on the iPad

It occurred to me the other day just how good it would due to have the slide shows that I used for training on the iPads of the students.

Now email the PDF file to your iPad, or to yourself if it has the same email address as your computer! When the email arrives click on the attachment PDF and wait while it downloads and opens. Then chose view it in iBooks.

The PDF file will now be in your iBooks PDF collection.

But how?

Well the slide shows are made in Keynote, and can be exported as PDF files. Use File > Print > PDF and Save As… put the file on your Desktop where it is easy to find later.Now email the PDF file to your iPad, or to yourself if it has the same email address as your computer! When the email arrives click on the attachment PDF and wait while it downloads and opens. Then chose view it in iBooks.

The PDF file will now be in your iBooks PDF collection.

Use iTunes sync

Alternatively, add the PDF file directly to your iTunes library, Book section. Go there and check the title and author are ok, then sync your iPad. If you are on iOS5 and iCloud your iPad will sync automatically by WiFi when you plug it into a USB power source.Friday 2 December 2011

Take the winds out of the financial sails

I am not a banker, and they will probably call this fanciful, but I do think we need to take the wind out of bank's sails, and make them subservient to national sovereignty, and better protector of OUR money. So,

Let's cap the interest on sovereign debt, to 4% say for everyone in the EU, and extend it all to 20 years. This means some will pay more (UK, Germany, France…) and some will pay less. Let the central banks smooth that out by issuing money to stop bank failures and by them seeking productive investments, let governments handle it by sweeping tax cuts so people spend.

In addition force fiscal inion of ALL 27 countries, including UK. Restructure the EU, yes I mean the EU, not the euro zone. Integrate more the politics and political decision making, let this control major fiscal policy, allowing freedom for local financing or taxes. But keep the banks small and local to prevent the "too big to fail" problem.

Stop the gambling and interbank shilly shallying. Allow CDS only to first level, but insist backed by secure assets, like gold.

Let's cap the interest on sovereign debt, to 4% say for everyone in the EU, and extend it all to 20 years. This means some will pay more (UK, Germany, France…) and some will pay less. Let the central banks smooth that out by issuing money to stop bank failures and by them seeking productive investments, let governments handle it by sweeping tax cuts so people spend.

In addition force fiscal inion of ALL 27 countries, including UK. Restructure the EU, yes I mean the EU, not the euro zone. Integrate more the politics and political decision making, let this control major fiscal policy, allowing freedom for local financing or taxes. But keep the banks small and local to prevent the "too big to fail" problem.

Stop the gambling and interbank shilly shallying. Allow CDS only to first level, but insist backed by secure assets, like gold.

Subscribe to:

Posts (Atom)